11 Mar Declining Balance Depreciation Calculation Example

Save more by mixing and matching the bookkeeping, tax, and consultation services you need. The beginning of period (BoP) book value of the PP&E for Year 1 is linked to our purchase cost cell, i.e. Per guidance from management, the PP&E will have a useful life of 5 years and a salvage value of $4 million. Calculate the depreciation of the asset mentioned in the above examples for the 3rd year.

Sample Full Depreciation Schedule

- Accumulated depreciation is total depreciation over an asset’s life beginning with the time when it’s put into use.

- As you might expect, the same two balance sheet changes occur, but this time, a gain of $7,000 is recorded on the income statement to represent the difference between the book and market values.

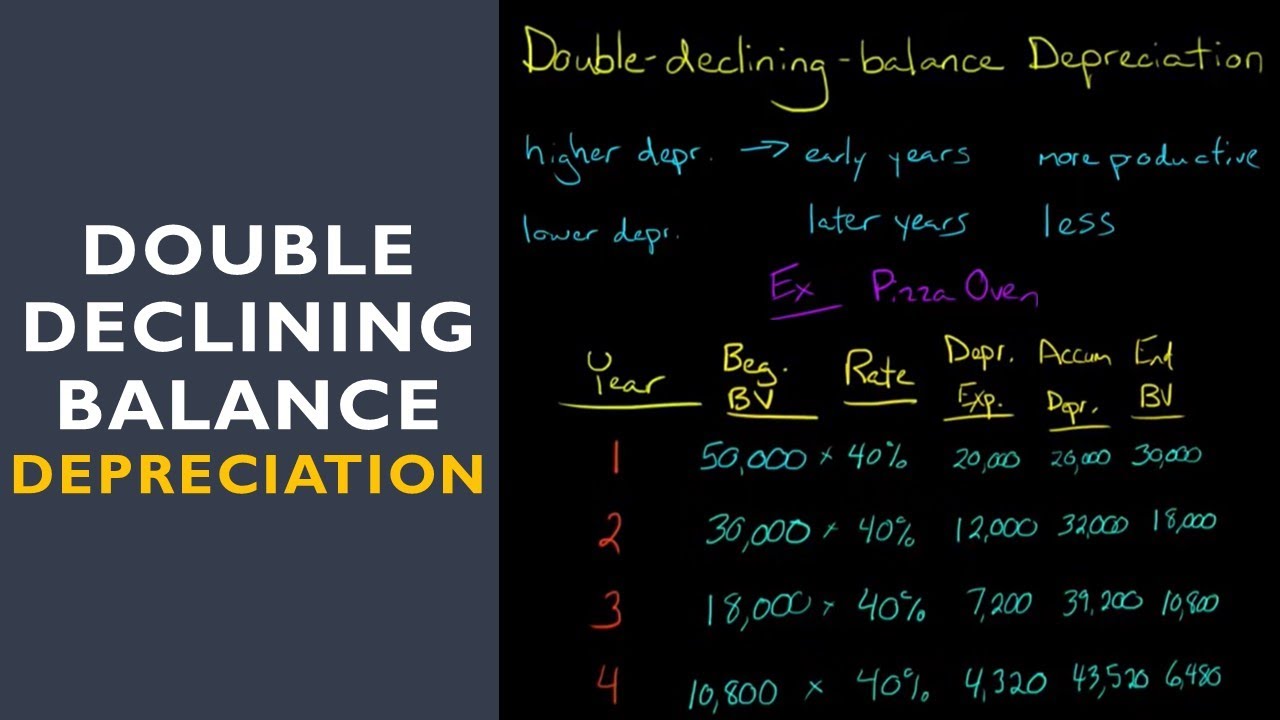

- Note that the depreciation in the fifth and final year is only for $1,480, rather than the $3,240 that would be indicated by the 40% depreciation rate.

- Assets that face a relatively high risk of technological obsolescence progressively decrease the competitive advantage a company can gain from their use.

- Adam received his master’s in economics from The New School for Social Research and his Ph.D. from the University of Wisconsin-Madison in sociology.

Certain fixed assets are most useful during their initial years and then wane in productivity over time, so the asset’s utility is consumed at a more rapid rate during the earlier phases of its useful life. For example, your company just bought the computers amount USD 10,000 and the depreciation rate for the computers, based on the company policy 50% reducing balance (declining balance). windfall tax noun american english definition and synonyms As under reducing balance method assets are depreciated at a faster rate in the early stage of their useful life, it is a more suitable method for assets that have greater utility in the earlier years. A better method for depreciating assets whose utility progressively increases is the Sum of the Digits Method. To start, a company must know an asset’s cost, useful life, and salvage value.

How can Taxfyle help?

Its sale could portray a misleading picture of the company’s underlying health if the asset is still valuable. The declining balance method is an accelerated depreciation system of recording larger depreciation expenses during the earlier years of an asset’s useful life. The system records smaller depreciation expenses during the asset’s later years. While the straight-line depreciation method is straight-forward and most popular, there are instances in which it is not the most appropriate method. Assets are usually more productive when they are new, and their productivity declines gradually due to wear and tear and technological obsolescence.

Declining Balance Depreciation Method

For reporting purposes, accelerated depreciation results in the recognition of a greater depreciation expense in the initial years, which directly causes early-period profit margins to decline. The prior statement tends to be true for most fixed assets due to normal “wear and tear” from any consistent, constant usage. Last year’s depreciation expenses are the difference between the net book value of the second year and the scrap value. The last year’s depreciation is normally different from the NBV of the year before last year with scrap value. The following is the example and it might help to illustrate the above explanation.

AccountingTools

If the beginning book value is equal (or almost equal) with the salvage value, don’t apply the DDB rate. Instead, compute the difference between the beginning book value and salvage value to compute the depreciation expense. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. A company estimates an asset’s useful life and salvage value (scrap value) at the end of its life.

Effects of the Declining Balance Method

You also want less than 200% of the straight-line depreciation (double-declining) at 150% or a factor of 1.5. Taxes are incredibly complex, so we may not have been able to answer your question in the article. Get $30 off a tax consultation with a licensed CPA or EA, and we’ll be sure to provide you with a robust, bespoke answer to whatever tax problems you may have. Implement our API within your platform to provide your clients with accounting services. Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts.

Hence, the declining balance depreciation is suitable for the fixed assets that provide bigger benefits in the early year. On the other hand, if the fixed asset provides the same or similar benefits each year to the company through its useful life, such as building, the straight-line depreciation will be more suitable in this case. The final step before our depreciation schedule under the double declining balance method is complete is to subtract our ending balance from the beginning balance to determine the final period depreciation expense. Even if the double declining method could be more appropriate for a company, i.e. its fixed assets drop off in value drastically over time, the straight-line depreciation method is far more prevalent in practice. The Double Declining Balance Method (DDB) is a form of accelerated depreciation in which the annual depreciation expense is greater during the earlier stages of the fixed asset’s useful life. Calculating the depreciation expenses using the reducing balance method is not too difficult.

Under this method, a constant depreciation rate is applied to an asset’s (declining) book value each year. This method results in accelerated depreciation and higher depreciation values in the early years of the life of an asset. Declining Balance Depreciation is an accelerated cost recovery (expensing) of an asset that expenses higher amounts at the start of an assets life and declining amounts as the class life passes.